Over the last several years, household debt across the world has been slowly increasing. That debt includes mortgages, car loans, and credit card debt. China’s household debt now stands at 49.1% of GDP, relatively low compared to many developed nations, but worrisome because of its 30 percentage point increase in the last decade. Shockingly, Switzerland leads the world with household debt at 127.5% of Gross Domestic Product. That means, for every $100,000 of GDP a household produces, they hold $127,500 in debt!

The average citizen in Switzerland, which has traditionally been an extremely wealthy country, has substantial assets (net worth) underpinning this debt, or at least four times more assets than the average American.

Even so, Switzerland, as well as nine other economies including Canada, Finland, and Australia, have debt levels that are high and rising quickly, at a pace that mirrors that of the US right before the housing bubble.

About this time every year, I get the travel itch. It’s the feeling that I need to book a trip for my family so we can go somewhere we’ve never been before, see something new, or just get out of the daily grind. Winter feels long, and the beautiful beach pictures in Instagram are calling me.

Yesterday, my friend sent me a picture of the little town in Northeastern Spain they’ll be visiting this summer. I. want. to. go.

However, our family just moved 1000 miles away to a new state last year, we bought a new house, and we have spent plenty of money on it. Plus, I’m not bringing in a steady income, since I’m taking a year off teaching to help us get settled, so it’s hard to justify setting aside thousands of our savings for a big trip (how much should you spend on travel, anyway? Answers here).

I’m not giving up so easily, however. Here are five ways I’m planning to save up for travel.

1. Save the Extra

This is about as obvious a tip as they come, but it’s not always easy to follow. This year, every single extra check, refund, tutoring payment, or gift is going straight to a fund called “Trips.”

In our Capital One Savings account, we have several subaccounts where we save for different goals. In our “Trips” fund, I’ll be saving all of the extra money we get, immediately, before I even have a chance to think otherwise.

I deposit any checks using my mobile app, then immediately transfer that amount from my bank to our Capital One subaccount.

The trick is to deposit the money immediately into an account or fund you can’t access or won’t let yourself touch.

It’s too easy to put the money in your general account, and attempt to save what’s left over at the end of the month. But in my house, that money will get spent, so I need to set it aside as quickly as possible to save for travel.

I have a problem. Yes, I’ll admit it. If you know me IRL, I’m sure you’ve heard me talk about it as it plagues me frequently. The problem is this: I occasionally panic because I think my kids aren’t doing enough activities.

I’ve suffered through the same conversation with myself for years (What? You don’t have conversations with yourself in your head?). It goes something like this:

Me: The boys aren’t signed up for any activities right now.

Myself: That’s ok, they’re doing deeply creative things at home.

Me: But X’s kids are on swim team. My kids should be on the swim team! They’ll learn discipline there, and focus, by being a part of something difficult that will stretch them. And both of them love swimming!

Myself: You’re doing it again.

Me: I KNOW! But Y’s kids play in tennis championships. The boys should join our tennis academy. It’s a family sport that they can play forever! I want them to be good at something, to have a skill. What kind of parent am I if I haven’t helped them develop a sport they love to play?

Myself: There’s still time.

Me: They’re getting older. I didn’t really play a sport when I was young. But I started running with my dad when I was 9! I haven’t run with the boys at all. They’re inside too much. They play too many electronics!

Myself: Junior ThreeYear has climbing.

Me: I know! But that’s only once per week. And is he really learning anything there? It’s a very basic group. Can I help him get better? Should he be going more? Now what do I do? More climbing, swimming, tennis? Which one to pick? They’re all so expensive. And they take up a lot of time. Maybe I’ll start with tennis lessons? Maybe karate would be a better choice…

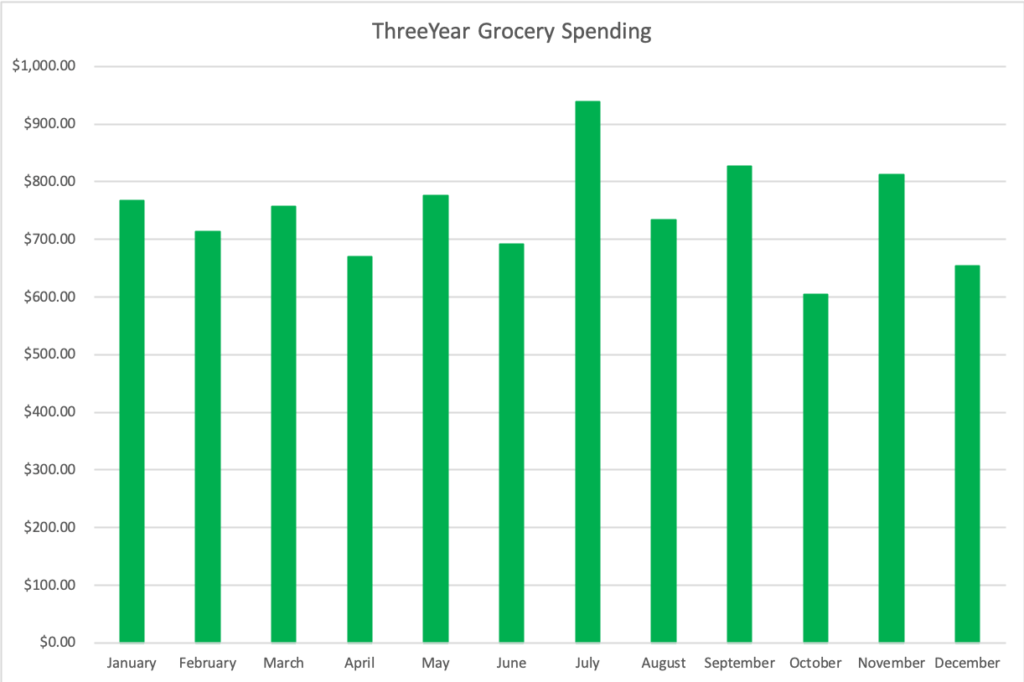

A year ago, I made a decision to try again: I’d been working to decrease our grocery bill for 10 years. I’d never been consistently successful at it, and as our family grew and our boys ate more, the grocery bill steadily ticked upward. In 2017, we spent almost $1000 per month on groceries alone. So I set a modest goal for 2018–to shave about 20% off our grocery bill each and every month. I set a budget of $772 per month, or $9264 in total yearly spending.

Did we do it? Well, despite going over budget in 4 of the last 12 months, we had an average monthly spend of $746.55 and a total yearly spend of $8958.60! We did it!!!

We did not halve our grocery bill. We did not keep it under $500. Or $400. Or $350. But we did hit and surpass our goal, keeping grocery spending to under $750 on average for the entire year.

I am proud. I am pleased. I have $1600 in the bank that I wouldn’t have had if I’d spent it on groceries, many of which we might have thrown away. I would have had $2400 if I’d saved $200 for each and every month of the year like I planned, but for four months in there, the months when we were getting our house ready to sell, I didn’t save the $200.

So what lessons can I extrapolate from this year-long experiment so that I can continue to spend less on our groceries?

Little ThreeYear and I spent a little time counting our blessings yesterday as we talked about his New Year’s Resolution, to work on his anger issues. Sweet thing, he hardly has any anger issues. He has major anxiety and sometimes that causes him to freak out a little. But he’s gotten so much better this year! So we talked about that and about all he’s good at, and all we’ve got to be thankful for. And I spent time counting my blessings after reading Mr. Money Mustache’s really honest and thoughtful post on his divorce.

Mr. ThreeYear and I have a best friend who’s a divorced, single-parent dad. For years, we watched many things happen with his former spouse and have seen the good, the bad, and the ugly that came from his divorce.

It takes such strength of character to be able to write about such a wrenching and difficult subject, with all its associated social baggage and judgment, in a way that’s designed to help others get better with money and life, and I admire MMM for writing about such a hard topic. I’ve read plenty of posts lately about people getting divorced, but not as many about staying married, and so here I humbly offer my own situation and lessons for better or for worse (no pun intended, of course).

The most helpful part of Pete’s post for me was where he gave tips on how to stay married. Staying married is really important to me. I remember in middle school, telling a classmate that I was never getting a divorce. She, with much more maturity and insight than I had at the time, reminded me that it wasn’t always within your control. I told her I’d do everything I could not to get divorced. I feel the same way twenty-eight years later.

My dad’s parents, my grandparents, got divorced after 34 years of marriage, and it kind of wrecked the family. It really messed up my aunt and uncle, who were born much younger than my dad. They were little kids at the time and got shuffled between two homes, one of which contained their mother who was losing her mind to grief and booze, and the other of which had their self-absorbed father who was more involved with his new wife than worried about his kids.

A year passes quickly, no? Especially when you move almost 1000 miles South during that year and upend your quiet life drastically. I’ve been fairly faithfully sharing our net worth and spending progress in 2018, so this final post of the year probably won’t be much of a surprise. Still, it’s fun to have a reminder of the good, bad, and ugly of this past year, and our final stopping place, net-worth wise.

Our Progress

Mr. ThreeYear receives his annual bonus in December. This year’s was a good one, which was helpful in offsetting some of the losses we experienced in the stock market. He used part of it to buy a new car, which you can read more about here, and is saving the rest. The deal this year was that he got to use the entire bonus however he wanted. As much as I’d love to take what’s left and throw it into our taxable account, I also love the fact that we’re at a place financially where the bonus truly is a bonus. For nine years, Mr. ThreeYear has dutifully turned over the bonus to me to put towards our financial goals. We’ve used it to save up for a downpayment on a house, increase our emergency fund, finance our trip to Chile, pay off our cars and Chile apartment, and many other things.

This year, he gets to enjoy the money and think up ways to spend it (he hates spending money, so I know him–he won’t actually spend it, he’ll just imagine dozens of ways to spend it.

So how much did we increase our net worth this year? Well…

This year, my #1 goal has been to lower my family’s grocery expenses from almost $1000 to no more than $772 each month.

For a lot of people, that number might seem huge. How do four people eat so much? For some people, that might seem like a ridiculously small amount. “How can they possibly subsist on so little?”

For me, grocery shopping is the thankless, difficult, necessary task that I do each and every week, going back again and again to the basics: meal planning, making lists, inventorying, not wasting food.

I love shopping at Aldi, the low-cost grocery store, but it’s 25 minutes away from my house, so getting there, buying groceries, and getting back to put them away can be a pain.

Enter: Instacart. A few weeks ago I saw a sign in Aldi that advertised grocery delivery with Instacart. For Aldi groceries! I was intrigued, and decided to spend the month of December testing the service out (because, with all of the running around and craziness in December, what better month to have groceries delivered straight to your door?

This is the end, my only friend… (cue The Doors music). We have reached the last few days of the year. You know why I love this time of year? Let me be honest:

presents. I love getting them, and I love giving them.

year-end bonus. Mr. ThreeYear gets his bonus in December so we have this whole chunk of extra money burning a hole in our pockets (okay, not really-it usually goes to worthy financial goals. But we still splurge a little with it).

Christmas music. It’s cozy and it reminds me of happy Christmases of yore (another totally holiday-appropriate word, yore is).

Family. I get to hang out with my extended family during the holidays.

New beginnings! The end of the year is the time when I’ve accomplished a lot of my goals, which gives me a happy, productive feeling, and then I have the excitement of creating a new goal sheet for the coming year.

While I gave you an update midyear , let’s see how I ended the year with these goals.

Last year, I published a guide for setting great goals in 2018. I thought it was worth revising for 2019. I’m excitedly setting goals for the coming year, and I have some great ideas brewing. This is the first year I’m goal setting for the blog, too! Enjoy your weekend, and if the mood strikes, put some goals to paper for 2019.

One thing is clear to me as we ride out the end of this year: if you set great goals for 2019, it will make a huge difference in what you’re able to accomplish next year. The world we live in today is practically designed to distract us from keeping our eyes on our most important goals and work (for example, as I’m typing this, I’m trying to ignore the loud cartoon my kids are watching across the room). So focus is key. And great goals help you keep your focus, all year long.

But how do you figure out the best goals to set for the upcoming year? Maybe you have fifteen burning desires that you’d love to achieve, but you don’t know how to prioritize them. Or maybe life is motoring along just fine, and you know you’d probably like to improve something, but you’re not sure what.

I found myself asking those exact same questions several years ago, and here’s what I’ve figured out really works when it’s time to goal set for the upcoming year.

1. Get Crystal Clear on your Values

It’s hard to prioritize your goals if you haven’t defined your values. What are your values, though? Values are what you judge to be the most important things in your life–the things that deep down, you care about the most. Given that definition, it seems like it would be easy to figure out your values. But it’s not always.

Sometimes, you want to value something that you actually don’t care about that much. For example, when I was in my 20s, I lived in Santiago, and Mr. ThreeYear and I were figuring out where we should go next. I was offered the opportunity to become part of an MBA program where I’d complete half in Chile and half at a great school in Texas. But I declined, ostensibly because I wanted to get into a top-10 MBA school, like Wharton. In the end, though, we moved back to the US and I didn’t go to an MBA school at all. To the shock of almost everyone in my family, I became a stay-at-home mom for seven-and-a-half years. It turns out that what I thought were my values–getting an MBA and climbing the corporate ladder–weren’t really my values at all. I really valued family, which was the real reason I didn’t stay in Chile to start an MBA, because I missed my family back in the US and wanted to go home. And I really valued motherhood, and making sure my children had a secure start in life.

Ahh, motherhood.

One of the best ways I’ve found to figure out your real values is the “What do I want?” exercise. It’s fairly simple. You take out a sheet of paper, and at the top, write, “What do I want?” Now, all you do is list the things you want. They can be as small and insignificant, or as large and pie-in-the-sky as you want. Anything that comes to mind goes on the list.

When you start this exercise, your first few wants will probably be fairly trivial and perhaps materialistic.

I moved from New Hampshire to North Carolina to get away from massive snowfall. And I did, honestly. My old town in New Hampshire suffered through a record three snow days in November, way before the snow normally starts. While things were chilly in Charlotte, the ground was brown, not white.

But, irony of ironies, Winter Storm Diego hit us a couple of weeks ago and not only did we have two snow days of our own, we got a solid week before the white stuff melted.

Honestly, I was kinda digging it. While I can’t make it through seven long months of white ground, seven days is manageable.

There’s something so cozy about winter. I find that in wintertime, December excluded, we tend to bunk down at home and spend more time together but less money. Probably because for the last few years, we’ve embraced the concept of hygge and home.

Hygge is, of course, the famous Danish concept of coziness. It’s the idea of making your home a warm and welcoming cave by lighting tea candles, building a great big fire (or turning up those gas logs), playing soothing music, and basically leaning in to the short, cold days of winter. Winter isn’t to be endured, according to the Danish, it’s to be embraced!

Since we only have to embrace a few months of cold weather (and it’s currently 55), I’m more than happy to enjoy what little truly cold weather we have, and transform our new house into a cozy nook.